Green Transformation and External Shocks: The Geoeconomics of Decarbonisation in the German Export Model

The “traffic light” coalition and gas

It is an image from what now feels like a distant past: then-Chancellor Olaf Scholz, Finance Minister Christian Lindner, and Economy Minister Robert Habeck stand in freezing temperatures in Wilhelmshaven in mid-December 2022, ceremonially opening Germany’s first “floating” Liquified Natural Gas (LNG) import terminal. This, Scholz declared, was a “very, very important contribution to our security,” following the abrupt halt of Russian gas supplies just months earlier.

A little over three years and four additional terminals later, that sense of security appears to be dissolving. A new study by the Institute for Energy Economics and Financial Analysis estimates that Europe’s dependence on a single LNG supplier could rise to as much as 80% in the worst-case scenario—within less than four years. This time, however, the issue is not Russia, but the United States, which under Donald Trump has been drifting toward authoritarianism. Repeated geopolitical threats from the White House toward Europe leave little doubt that this growing dependency could soon be weaponised.

How did this situation arise? In a study last year, we analysed how the Russian gas cutoff affected progress in decarbonisation—the systematic reduction of greenhouse gas emissions with the goal of achieving a climate-neutral economy—in Germany. We argued that such geoeconomic shocks have differentiated effects. While we viewed the enthusiasm for LNG shown by Habeck and others as problematic, we also observed positive effects, such as a long-term expansion of renewable energy capacity and declining energy intensity in industrial production.

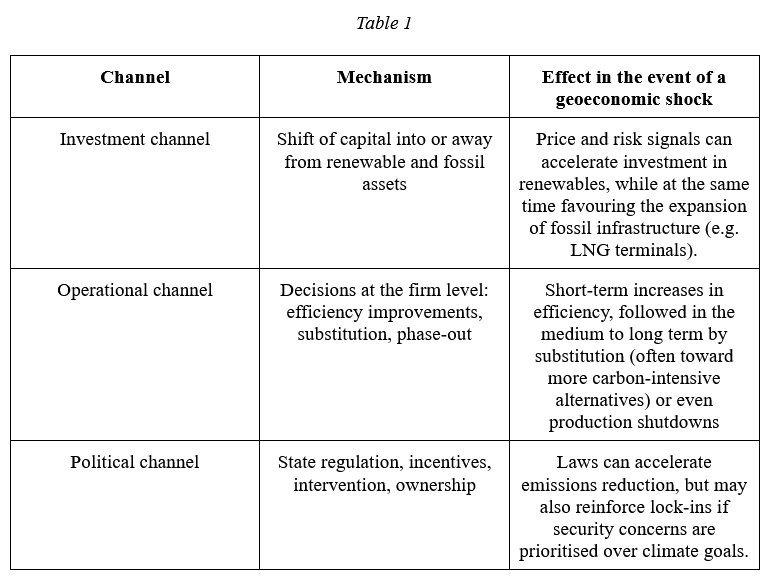

Geoeconomic shocks generally affect decarbonisation processes through several channels (see Table 1), particularly through investment decisions (does capital flow into renewables or fossil fuels?), operational decisions at the firm level (are efficiency or substitution measures implemented?), and political responses (do policymakers accelerate reforms or slow them down?).

In the German case, these effects were filtered through the country’s export-oriented growth model. A strong dependence on “cheap” Russian gas was generated not only by the buildings sector, but also—crucially—by export-oriented, energy-intensive industries. The chemical sector alone accounted for around 30 percent of industrial gas consumption in 2022. At the same time, more than half of Germany’s gas imports came from Russia.

We found that traditional manufacturing was less affected by the energy shock, whereas energy-intensive industries experienced sharp declines in production. This downward trend continued in subsequent years, culminating in a staggering 80% drop in investment in the European chemical industry by 2025. Rising energy prices have caused the German-European export engine to stagnate, increasingly being displaced by cheaper Chinese products.

Overall, while the gas supply shock produced some positive decarbonisation effects, these were diluted by political decisions aimed at preserving the German export model. This brings us back to the present—and to American LNG.

First as tragedy, then as farce

Germany’s—and more broadly Europe’s—response to the 2022 energy shock highlights the importance of analysing geoeconomic developments alongside green transformation conflicts. In retrospect, the attempt to balance potential independence from fossil fuel imports with the preservation of energy-intensive industry was not particularly successful.

The partial shift to LNG terminals has, in just three years and one U.S. election later, placed the EU and Germany at risk of a new and potentially serious dependency on the United States—even if Belgium, the Netherlands, and Norway remain larger suppliers for now. In hindsight, the conclusion is clear: had Germany pursued a rapid decarbonisation strategy instead of relying on LNG in 2022, the situation today might look very different. Pakistan’s recent “solar boom” offers a glimpse of such an alternative path.

How can this repetition of history—first as tragedy, now as farce—be explained? The German government, and Europe more broadly, underestimated the risk of “carbon lock-in,” a concept widely discussed in the academic literature. This refers to a specific form of path dependency: infrastructures, technologies, institutions, and behaviours built around fossil fuel dependence are difficult to dismantle.

In this sense, all modern capitalist economies are “locked in.” However, the specific form of this lock-in varies across growth models and determines how difficult it is to overcome this lock-in. Decarbonisation is therefore not merely a technical challenge but a political process of breaking these carbon lock-ins. Interests embedded in consumption and production patterns must be reorganised, compensated, or confronted—often at significant political cost.

In Germany’s case, dependence on Russian gas and reliance on industrial exports were closely intertwined. The pivot to LNG imports from Norway, Qatar, and the United States was a political solution whose risks were already well known—and documented. Carbon lock-in helps explain why these risks were ignored, and why changing geopolitical conditions are now generating renewed pressure.

Geoeconomics and transformation

A geoeconomic world—one in which states and firms increasingly use global interdependencies strategically—is not, at first glance, good news for the green transition. The shift of resources and political priorities toward defence and resilience often comes at the expense of ambitious transformation goals.

Yet the German case—from Russian dependence to looming dependence on US LNG—also reveals the limits of this zero-sum thinking. Decarbonisation is not only about costs and conflicts; it also reduces dependence on fossil fuel imports.

In this respect, Europe is not so different from China, which has historically been a net importer of fossil energy. However, Chinese policymakers quickly recognised that energy dependence is a liability in a geoeconomic world. Over the past three years, China alone has accounted for more than half of global solar capacity installations. Solar and wind capacity have tripled since the pandemic. In 2023 alone, China installed around 217 gigawatts of solar capacity—more than any other country had installed in total up to that point.

Of course, China’s success story also has a fossil dimension: emissions have risen almost in parallel with renewable expansion. Yet the strategic direction is clear: in a geoeconomic world, decarbonisation is not a burden but a prerequisite for strategic autonomy.

From shocks to strategy

A defining feature of the current transformation of the global economic order is the growing importance of geoeconomic shocks. These go far beyond energy imports. Disruptions in global supply chains and production networks do not merely produce price shocks—they affect entire production and growth models.

Depending on the sector and nature of the shock, the consequences for energy systems, sustainable production, and investment opportunities can be profound. In short, while decarbonisation remains a transnational challenge, the conditions under which it takes place are becoming more complex and uncertain.

A resilience-oriented policy must therefore learn to navigate this new form of strategic interdependence. Rather than treating decarbonisation and security as conflicting goals, European governments should focus more on their interaction. Based on our analytical framework, this implies:

- Public investment in renewable energy is crucial, both to generate economies of scale and to act as a multiplier for private investment. State-led investment vehicles can channel funds into rapid expansion of solar capacity, energy storage, and grid infrastructure, thereby strengthening system resilience.

- Firms are effective at improving energy efficiency, but often revert to fossil substitutions (e.g. coal instead of gas). Clear regulatory frameworks are needed to promote renewable substitution and prevent production shutdowns. Otherwise, fears of deindustrialisation and declining prosperity may fuel a “carbon backlash”—a shift in public support away from decarbonisation toward a seemingly safer fossil status quo. There is also the risk of “carbon leakage,” where energy-intensive production is relocated abroad, merely shifting emissions rather than reducing them.

- Political decision-making and power relations are decisive in determining whether a geoeconomic shock accelerates or hinders the energy transition—and whether it strengthens or weakens social security, democratic cohesion, and economic resilience. It is crucial to recognise that shocks do not merely disrupt otherwise stable systems; they expose fundamental structural weaknesses in existing growth models. An economy built on cheap fossil imports and export surpluses is unlikely to remain viable in a geoeconomic world. What is needed are proactive, systemic reforms that build long-term resilience and social cohesion.

________________________________

Editorial Note:

This article is produced as part of a collaboration between Rethinking Economics International, Makronom and the Economists for Future DE and was originally written in German language. The 2026 contributions engage with ongoing debates on anti-authoritarian and anti-fascist perspectives on economic policy, with particular attention to how social security arrangements can help counter authoritarian and nationalist tendencies. Contributions in this series also explore welfare state design, property relations, pension systems, and institutional reforms with a view to strengthening democratic cohesion, ecological stability, and economic resilience. The views expressed in this article are the author’s own and do not necessarily reflect those of the participating platforms.

About the authors:

Milan Babic is an associate professor of political economy at the University of Amsterdam. His research focuses on the transformation of the global political economy from a neoliberal order to a geo-economic one. In this context, he examines the interplay between the market and the state, corporate power in global capitalism, and the political economy of decarbonization. Milan can be found on Bluesky at @mbabic.bsky.social. His latest book, Geoökonomie, was published by Suhrkamp in May 2025.

Daniel Mertens is a political scientist and professor of International Political Economy at the Institute of Social Sciences at the University of Osnabrück. His research and teaching focus on the transformation of the global and European political economy, particularly with regard to financial, climate, and industrial policy. For more information on his research interests and publications, visit danielmertens.info.

________________________________________

{kind=link}